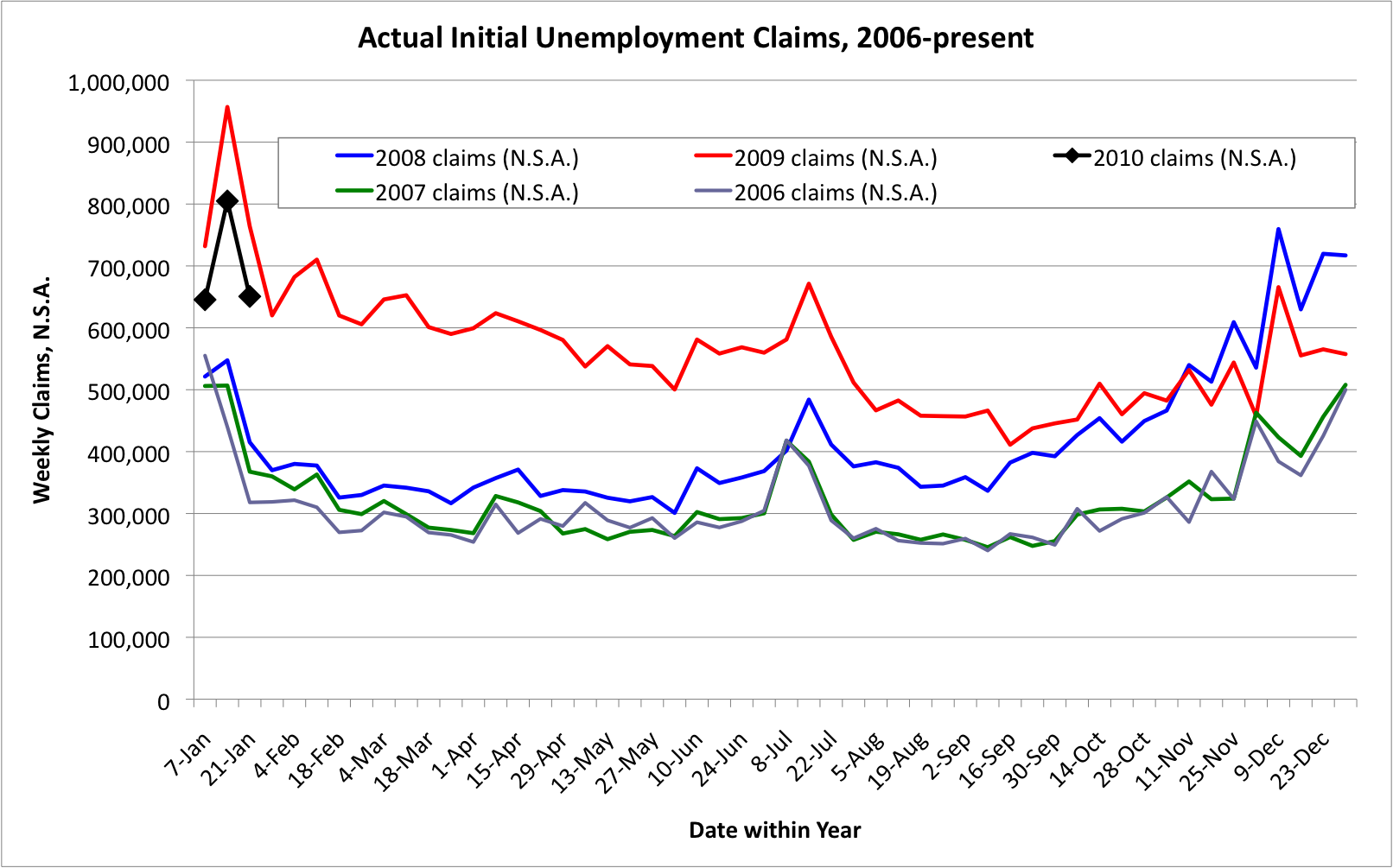

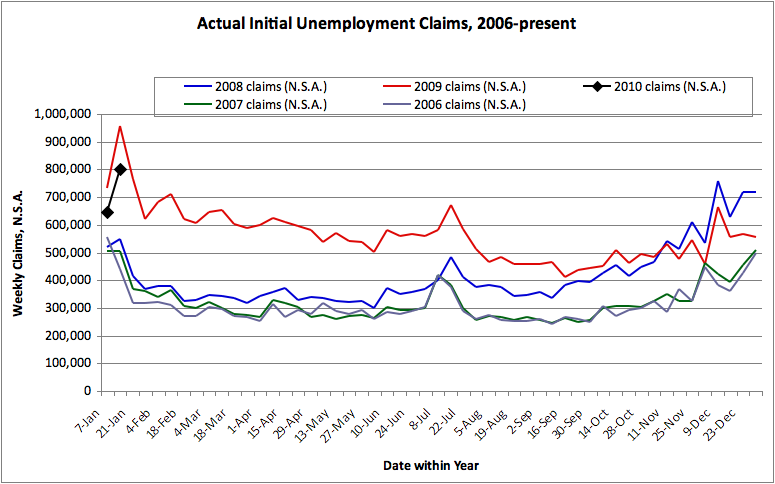

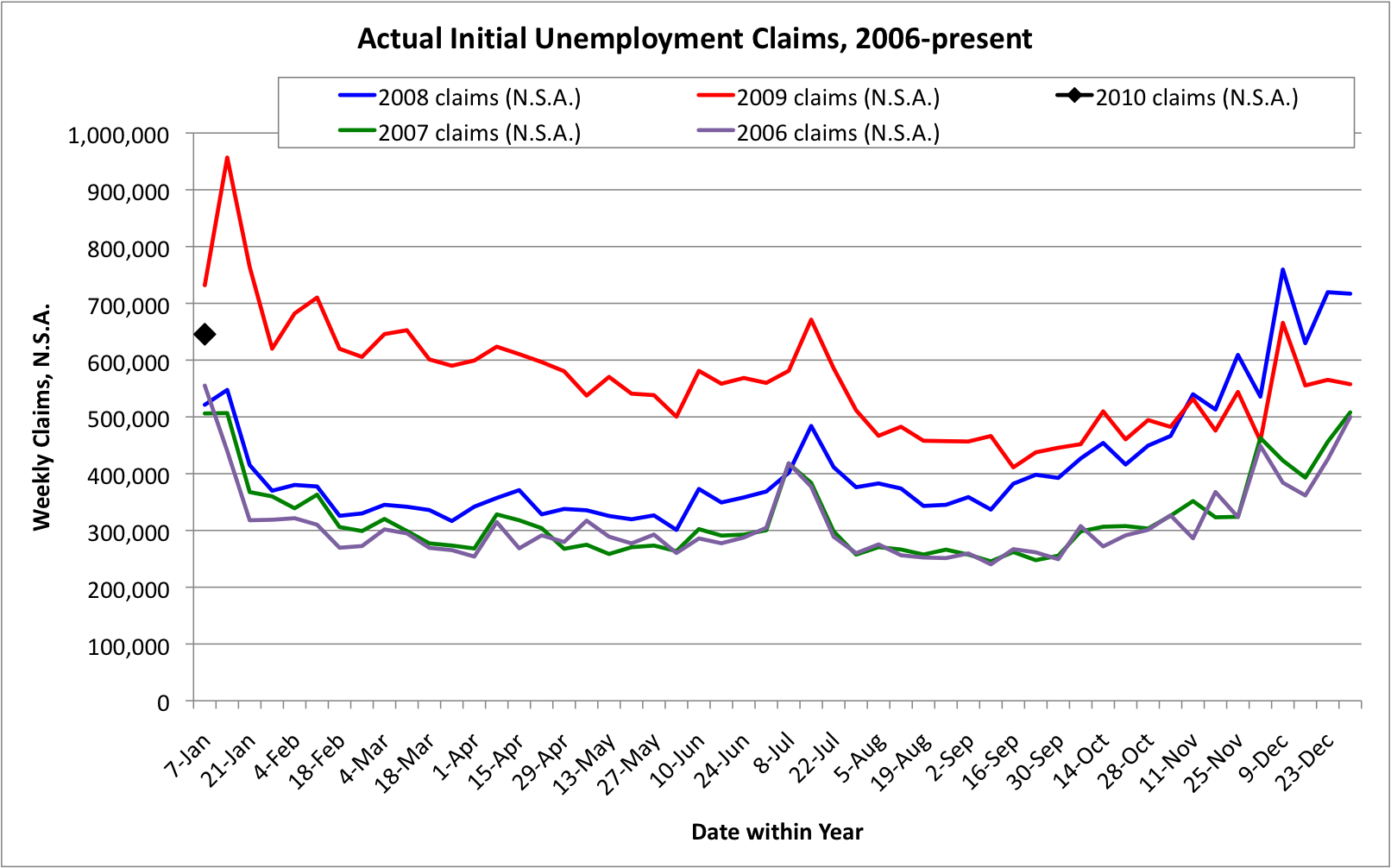

Apropos of the current fears of another market panic in 2010, and a new topic for Do Not Feed the Squid fans: “How can we arrange economic matters differently, so that we do not have another crisis, either soon, or ever?”

There was an interesting discussion of the concept of “Automatic Stabilizers” to provide countercyclical fiscal policy, but like all other policy responses I don’t think auto-spending plans or other “stabilizers” will help to prevent future financial excesses. Centuries of financial history, as retold in books such as “Manias, Panics and Crashes” by Kindleberger, tell us that crash-preventing and crash-mitigating policy constraints tend to be undone by the same economic and political forces that lead to the financial excesses. It is not enough to imagine stabilizers, they must be implemented, and they must be implemented in such a way that they remain effective without being evaded or gamed.

Perhaps the best stabilizer is a system which doesn’t tend to excess in the first place, so that the resulting crashes are not so severe. The Founding Fathers, within the constraints of the 1700s, were not unwise in this regard – Article 1 of the U.S. Constitution actually has the simplest of all financial stabilizers, demanding that only gold and silver coin may be used as tender for debts (Section 10), authorizing only Congress to borrow money on the credit of the United States (Section 8), empowering only Congress to coin money (Section 8), and that “No money shall be drawn from the treasury, but in consequence of appropriations made by law” (Section 9). Congress has managed to mismanage this. Why should they be expected not to muck up any other “automatic stabilizers”? (An interesting side note — the rest of the Constitution does not even mention money.)

Now, the 1800s had plenty of financial ups and downs, and politicians (seeking always to take credit for trying to make things better?) have muddled with the system, so that despite the constitution gold and silver coin are no longer money, Congress has delegated a lot of financial responsibility, and savers seeking to invest must deal with a lot more “political risk”… Meanwhile, financial crises still occur, and they are certainly more complex now, but are they any less severe?

This sort of thinking led me to the following rant, which I want to post here for posterity:

We HAD automatic stabilizers! But the problem with “automatic stabilizers” is that, in a credit mania, the political process leads to the dismantling of the stabilizers. How many defensive mechanisms were put in place after the Great Depression, and then dismantled in the 1990s and early 2000s, again? We had banks that could be “failed out” via the FDIC. We had Glass-Steagall separating speculation from honest lending. We had lenders who had to own the risks of their own lending, not pawn them off via “securitization” (what an oxymoron! no one was made secure!). We had a whole alphabet soup of regulatory agencies.

We HAD automatic stabilizers. But we threw them away! The regulators allowed both commercial and investment banks to hide toxic debts “off balance sheet” (as though, in reality, there could even be such a thing?). We let the banks leverage up well beyond historically prudent levels, ignoring centuries of financial history and thinking “it’s different in our time” (I.D.I.O.T. thinking). These failures were systemic and widespread and they did not come out of nowhere for no reason. They occurred because a long reign of prosperity had led to complacent outlooks. They occurred because an overly complex system was built up to hide the sausage, and the new system permitted trillions of dollars in hidden fraud (Galbraith’s “Bezzle”). They occurred because the people asking for the bending of the rules were making gobs of money, and the people who had the authority to say no, in far too many cases, were too interested in sharing in those gobs of money and not sufficiently interested in protecting the public interest. They occurred because too many people were too enthralled with fancy new marketing terms, and the few who were sufficiently quantitative and skeptical to realize that a “credit default swap” is the same as an insurance contract (and thus out to be regulated as such) were outvoted.

We had automatic stabilizers, and when we actually needed them, they weren’t there anymore. And probably in 60-80 years the automatic stabilizers that we will put in place will also be thrown away, and in 70-100 years there will another enormous crisis. Unless we truly do something different this time. But the gridlock in Washington and the entrenched resistance on Wall Street doesn’t give one any reason for optimism.

Why is it, again, that everyone who created this mess is still in power? Why are the same regulators now expected to actually enforce prudent fiscal responsibility, whose nonfeasance enabled the runaway banks to drive us to the brink of ruin? Why is the same clique of bankers still in charge of the “too big to fail” institutions, that failed and were bailed? Why are the same Congresspeople in charge, who failed to exercise their proper oversight of the executive branch agencies and ensure that regulation actually took place? Why is it that the Federal Reserve is being allowed to purchase outright securities that are not “full faith and credit” obligations of the United States Government, despite the very clear language in the Federal Reserve Charter limiting the Fed’s authority only to those securities? Where are the protests at the TARP vote (against the will of the vast majority of those willing to contact their Congress)? Where are the riots against the indentured servitude our children and grandchildren will face, paying interest on $15,000,000,000,000 in debt that they did not ask for and which does them no good? (Those used to be “astronomic” numbers… now they are “economics” numbers!)

Oh… we haven’t DEMANDED either manual OR automatic stabilizers, yet.

The crisis will continue until the national response improves.

{kind=link}